Week 6 Discussion

Haley Romeros had just been appointed vice president of the Rocky Mountain Region of the Bank Services Corporation (BSC). The company provides check processing services for small banks. The banks send checks presented for deposit or payment to BSC, which records the data on each check in a computerized database. BSC then sends the data electronically to the nearest Federal Reserve Bank check-clearing center where the appropriate transfers of funds are made between banks. The Rocky Mountain Region has three check processing centers, which are located in Billings, Montana; Great Falls, Montana; and Clayton, Idaho.

Prior to her promotion to vice president, Ms. Romeros had been the manager of a check processing center in New Jersey. Immediately after assuming her new position, Ms. Romeros requested a complete financial report for the just-ended fiscal year from the region’s controller, John Littlebear. Ms. Romeros specified that the financial report should follow the standardized format required by corporate headquarters for all regional performance reports.

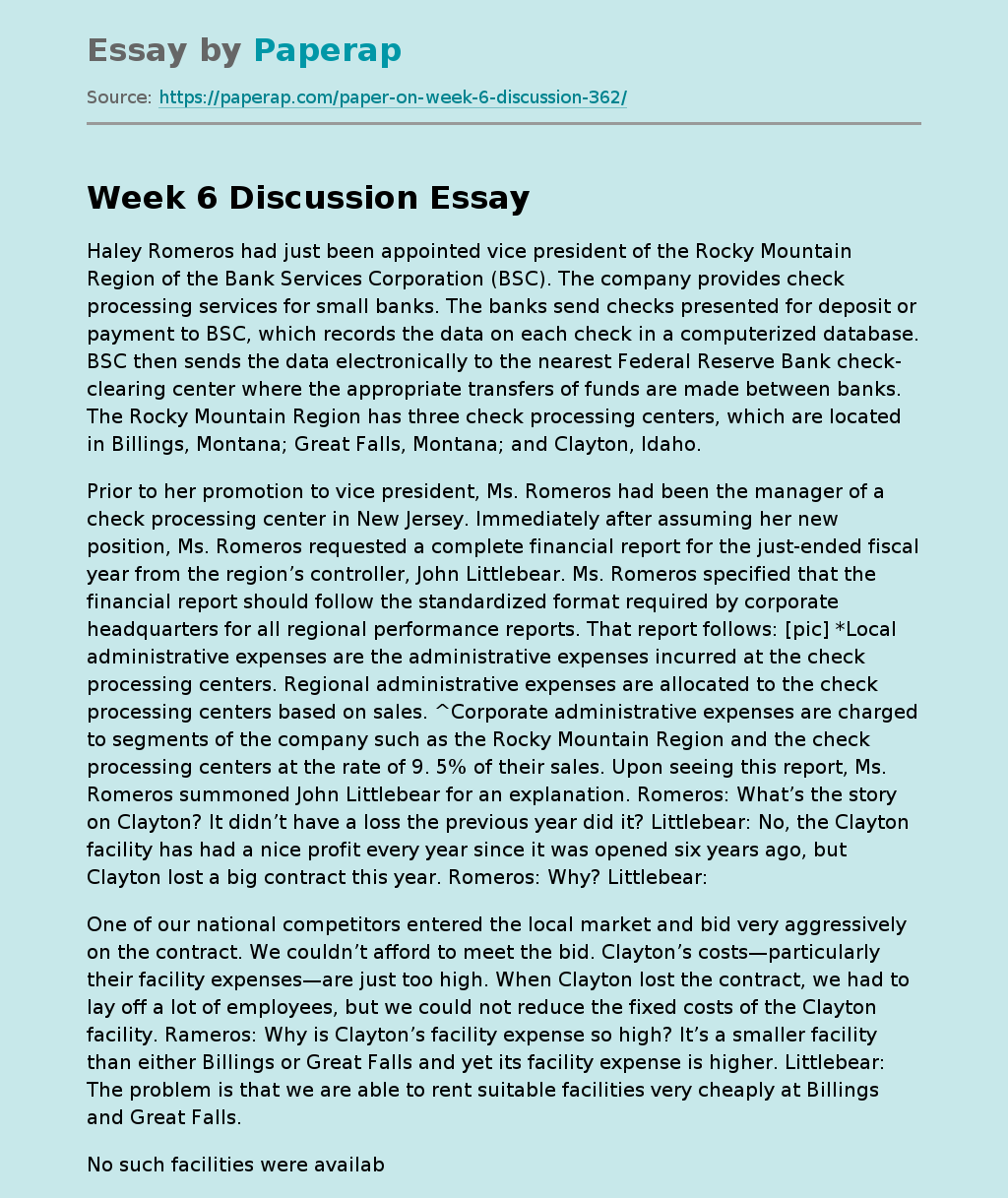

That report follows: [pic] *Local administrative expenses are the administrative expenses incurred at the check processing centers. Regional administrative expenses are allocated to the check processing centers based on sales. ^Corporate administrative expenses are charged to segments of the company such as the Rocky Mountain Region and the check processing centers at the rate of 9. 5% of their sales. Upon seeing this report, Ms. Romeros summoned John Littlebear for an explanation. Romeros: What’s the story on Clayton? It didn’t have a loss the previous year did it? Littlebear: No, the Clayton facility has had a nice profit every year since it was opened six years ago, but Clayton lost a big contract this year.

5 (234)

5 (234)

“ Very organized ,I enjoyed and Loved every bit of our professional interaction ”

Romeros: Why? Littlebear:

One of our national competitors entered the local market and bid very aggressively on the contract. We couldn’t afford to meet the bid. Clayton’s costs—particularly their facility expenses—are just too high. When Clayton lost the contract, we had to lay off a lot of employees, but we could not reduce the fixed costs of the Clayton facility. Rameros: Why is Clayton’s facility expense so high? It’s a smaller facility than either Billings or Great Falls and yet its facility expense is higher. Littlebear: The problem is that we are able to rent suitable facilities very cheaply at Billings and Great Falls.

No such facilities were available at Clayton; we had them built. Unfortunately, there were big cost overruns, The contractor we hired was inexperienced at this kind of work and in fact went bankrupt before the project was completed. After hiring another contractor to finish the work, we were way over budget. The large depreciation charges on the facility didn’t matter at first because we didn’t have much competition at the time and could charge premium prices. Rorneros: Well we can’t do that anymore. The Clayton facility will obviously have to be shut down. Its business can be shifted to the other two check processing centers in the region.

Littlebear: I would advise against that. The $1,200,000 in depreciation at the Clayton facility is misleading. That facility should last indefinitely with proper maintenance. And it has no resale value; there is no other commercial activity around Clayton. Romeros: What about the other costs at Clayton? Littlebear: If we shifted Clayton’s business over to the other two processing centers in the region, we wouldn’t save anything on direct labor or variable overhead costs. We might save $90,000 or so in local administrative expense, but we would not save any regional administrative expense and corporate headquarters would still charge us 9. % of our sales as corporate administrative expense. In addition, we would have to rent more space in Billings and Great Falls in order to handle the work transferred from Clayton; that would probably cost us at least $600,000 a year. And don’t forget that it will cost us something to move the equipment from Clayton to Billings and Great Falls. And the move will disrupt service to customers. Rorneros: I understand all of that, but a money-losing processing center on my performance report is completely unacceptable. Littlebear: And if you shut down Clayton, you are going to throw some loyal employees out of work.

Romeros: That’s unfortunate, but we have to face hard business realities. Littlebear: And you would have to write off the investment in the facilities at Clayton. Romeros: I can explain a write-off to corporate headquarters; hiring an inexperienced contractor to build the Clayton facility was my predecessor’s mistake. But they’ll have my head at headquarters if I show operating losses every year at one of my processing centers. Clayton has to go. At the next corporate board meeting, I am going to recommend that the Clayton facility be closed. Required: 1.

From the standpoint of the company as a whole, should the Clayton processing center be shut down and its work redistributed to other processing centers in the region? Explain. 2. Do you think Haley Romeros’s decision to shut down the Clayton facility is ethical? Explain. 3. What influence should the depreciation on the facilities at Clayton have on prices charged by Clayton for its services? SOLUTION: 1. The original cost of the facilities at Clayton is a sunk cost and should be ignored in any decision. The decision being considered here is whether to continue operations at Clayton.

The only relevant costs are the future facility costs that would be affected by this decision. If the facility were shut down, the Clayton facility has no resale value. In addition, if the Clayton facility were sold, the company would have to rent additional space at the remaining processing centers. On the other hand, if the facility were to remain in operation, the building should last indefinitely, so the company does not have to be concerned about eventually replacing it. Essentially, there is no real cost at this point of using the Clayton facility despite what the financial performance report indicates.

Indeed, it might be a better idea to consider shutting down the other facilities because the rent on those facilities might be avoided. The costs that are relevant in the decision to shut down the Clayton facility are: |Increase in rent at Billings and Great Falls |$600,000 | |Decrease in local administrative expenses | (90,000) | |Net increase in costs |$510,000 |

In addition, there would be costs of moving the equipment from Clayton and there might be some loss of sales due to disruption of services. In sum, closing down the Clayton facility would almost certainly lead to a decline in BSC’s profits. Even though closing down the Clayton facility would result in a decline in overall company profits, it would result in an improved performance report for the Rocky Mountain Region (ignoring the costs of moving equipment and potential loss of revenues from disruption of service to customers). Financial Performance | |After Shutting Down the Clayton Facility | |Rocky Mountain Region | | |Total | |Sales |$50,000,000 | |Selling and administrative expenses: | | |Direct labor 32,000,000 | |Variable overhead |850,000 | |Equipment depreciation |3,900,000 | |Facility expense* |2,300,000 | |Local administrative expense** |360,000 | |Regional administrative expense |1,500,000 | |Corporate administrative expense | 4,750,000 | |Total operating expense | 45,660,000 | |Net operating income |$ 4,340,000 | * $2,800,000 – $1,100,000 + $600,000 = $2,300,000 ** $450,000 – $90,000 = $360,000 2. If the Clayton facility is shut down, BSC’s profits will decline, employees will lose their jobs, and customers will at least temporarily suffer some decline in service. Therefore, Romeros is willing to sacrifice the interests of the company, its employees, and its customers just to make her performance report look better. While Romeros is not a management accountant, the Standards of Ethical Conduct for Management Accountants still provide useful guidelines.

By recommending closing the Clayton facility, Romeros will have to violate the Credibility Standard, which requires the disclosure of all relevant information that could reasonably be expected to influence an intended user’s understanding of the reports, analyses, or recommendation. Presumably, if the corporate board were fully informed of the consequences of this action, they would disapprove. In sum, it is difficult to describe the recommendation to close the Clayton facility as ethical behavior. In Romeros’ defense, however, it is not fair to hold her responsible for the mistake made by his predecessor. It should be noted that the performance report required by corporate headquarters is likely to lead to other problems such as the one illustrated here.

The arbitrary allocations of corporate and regional administrative expenses to processing centers may make other processing centers appear to be unprofitable even though they are not. In this case, the problems created by these arbitrary allocations were compounded by using an irrelevant facilities expense figure on the performance report. 3. Prices should be set ignoring the depreciation on the Clayton facility. As argued in part (1) above, the real cost of using the Clayton facility is zero. Any attempt to recover the sunk cost of the original cost of the building by charging higher prices than the market will bear will lead to less business and lower profits.

Week 6 Discussion. (2017, Dec 06). Retrieved from https://paperap.com/paper-on-week-6-discussion-362/