California Creamery

The following academic paper highlights the up-to-date issues and questions of California Creamery. This sample provides just some ideas on how this topic can be analyzed and discussed.

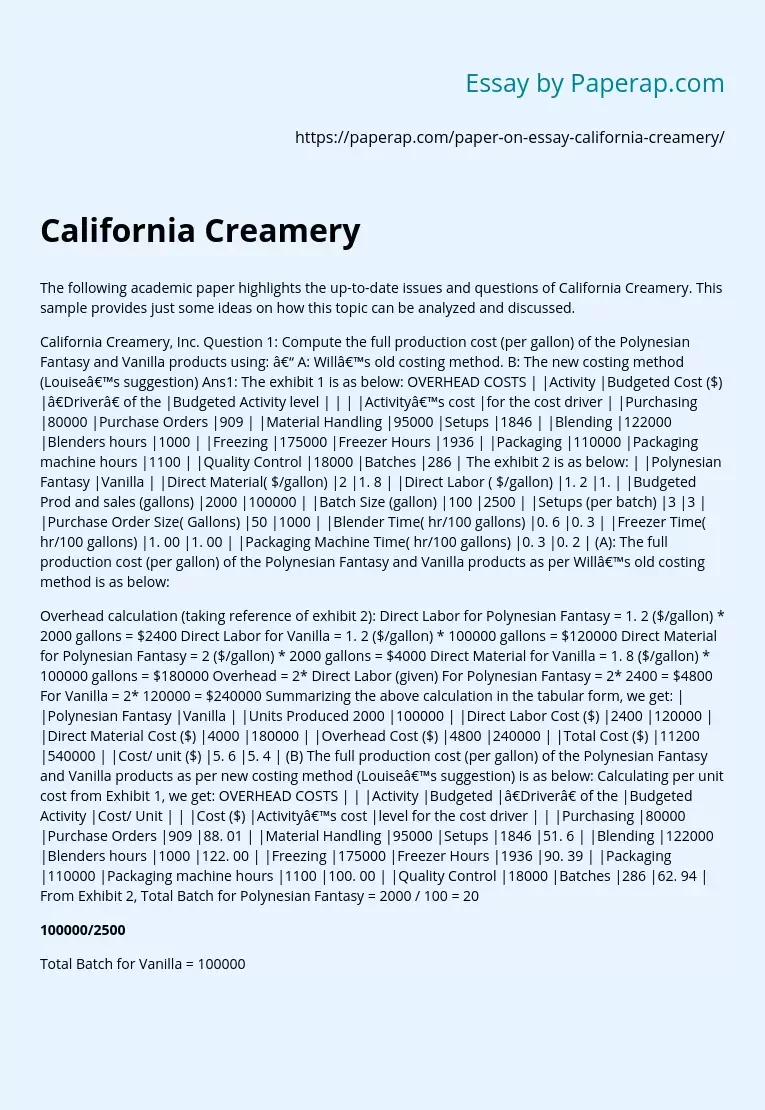

California Creamery, Inc. Question 1: Compute the full production cost (per gallon) of the Polynesian Fantasy and Vanilla products using: – A: Will’s old costing method. B: The new costing method (Louise’s suggestion) Ans1: The exhibit 1 is as below: OVERHEAD COSTS | |Activity |Budgeted Cost ($) |”Driver” of the |Budgeted Activity level | | | |Activity’s cost |for the cost driver | |Purchasing |80000 |Purchase Orders |909 | |Material Handling |95000 |Setups |1846 | |Blending |122000 |Blenders hours |1000 | |Freezing |175000 |Freezer Hours |1936 | |Packaging |110000 |Packaging machine hours |1100 | |Quality Control |18000 |Batches |286 | The exhibit 2 is as below: | |Polynesian Fantasy |Vanilla | |Direct Material( $/gallon) |2 |1.

8 | |Direct Labor ( $/gallon) |1. 2 |1. | |Budgeted Prod and sales (gallons) |2000 |100000 | |Batch Size (gallon) |100 |2500 | |Setups (per batch) |3 |3 | |Purchase Order Size( Gallons) |50 |1000 | |Blender Time( hr/100 gallons) |0. 6 |0. 3 | |Freezer Time( hr/100 gallons) |1. 00 |1. 00 | |Packaging Machine Time( hr/100 gallons) |0. 3 |0. 2 | (A): The full production cost (per gallon) of the Polynesian Fantasy and Vanilla products as per Will’s old costing method is as below:

Overhead calculation (taking reference of exhibit 2): Direct Labor for Polynesian Fantasy = 1.

2 ($/gallon) * 2000 gallons = $2400 Direct Labor for Vanilla = 1. 2 ($/gallon) * 100000 gallons = $120000 Direct Material for Polynesian Fantasy = 2 ($/gallon) * 2000 gallons = $4000 Direct Material for Vanilla = 1. 8 ($/gallon) * 100000 gallons = $180000 Overhead = 2* Direct Labor (given) For Polynesian Fantasy = 2* 2400 = $4800 For Vanilla = 2* 120000 = $240000 Summarizing the above calculation in the tabular form, we get: | |Polynesian Fantasy |Vanilla | |Units Produced 2000 |100000 | |Direct Labor Cost ($) |2400 |120000 | |Direct Material Cost ($) |4000 |180000 | |Overhead Cost ($) |4800 |240000 | |Total Cost ($) |11200 |540000 | |Cost/ unit ($) |5. 6 |5. 4 | (B) The full production cost (per gallon) of the Polynesian Fantasy and Vanilla products as per new costing method (Louise’s suggestion) is as below: Calculating per unit cost from Exhibit 1, we get: OVERHEAD COSTS | | |Activity |Budgeted |”Driver” of the |Budgeted Activity |Cost/ Unit | | |Cost ($) |Activity’s cost |level for the cost driver | | |Purchasing |80000 |Purchase Orders |909 |88.

5 (876)

5 (876)

“ Have been using her for a while and please believe when I tell you, she never fail. Thanks Writer Lyla you are indeed awesome ”

01 | |Material Handling |95000 |Setups |1846 |51. 6 | |Blending |122000 |Blenders hours |1000 |122. 00 | |Freezing |175000 |Freezer Hours |1936 |90. 39 | |Packaging |110000 |Packaging machine hours |1100 |100. 00 | |Quality Control |18000 |Batches |286 |62. 94 | From Exhibit 2, Total Batch for Polynesian Fantasy = 2000 / 100 = 20

100000/2500

Total Batch for Vanilla = 100000 / 2500 = 40 Total Material Handling setup (per batch) for Polynesian Fantasy = 20 * 3 = 60 Total Material Handling setup (per batch) for Vanilla = 40 * 3 = 120 Total purchase orders for Polynesian Fantasy = 2000 / 50 = 40 Total purchase orders for Vanilla = 100000 / 1000 = 100 Total Blending time (Hrs) for Polynesian Fantasy = (2000 * 0. 6)/100 = 12 Hrs Total Blending time (Hrs) for Vanilla = (100000 * 0. 3) / 100 = 300 Hrs Total freezing time (Hrs) for Polynesian Fantasy = (2000 * 1) / 100 = 20 Hrs Total freezing time (Hrs) for Vanilla = (100000 * 1) / 100 = 1000 Hrs Total Packaging time (Hrs) for Polynesian Fantasy = (2000 * 0. ) / 100 = 6 Total Packaging time (Hrs) for Vanilla = (100000 * 0. 2) / 100 = 200 Using the above details and per unit cost calculated from exhibit 1, the overhead costs for both the products are as under: | OVERHEAD DETAILS |Polynesian Fantasy |Vanilla | |Purchase overhead |3520. 35 |8800. 88 | |($88. 01 * purchase order) | | | |Blending Overhead |1464. 00 |36600. 0 | |($122 * Blending time) | | | |Freezing Overhead |1807. 85 |90392. 56 | |($90. 39 * freezing time) | | | |Packaging Overhead |600. 00 |20000. 00 | |($100 * packaging time) | | | |Quality Overhead |1258. 74 |2517. 48 | |($62. 4 * number of batches) | | | |Material Handling Setup |3087. 76 |6175. 51 | |($51. 46 * total setup) | | | |TOTAL |11738. 70 |164486. 44 | The Direct Cost for both the products is as under: |DIRECT COST DETAILS |Polynesian Fantasy |Vanilla | |Total Direct Labor |2400 |120000 | |($1. * Budgeted Production and sales) | | | |Total Direct Material |4000 |180000 | |($2 * Budgeted Production and sales) | | | |TOTAL |6400 |300000 | Therefore, Total cost for Polynesian Fantasy = $11738. 70 + $ 6400 = $ 18138. 70 And, per unit cost for Polynesian Fantasy = $ 18138. 70 / 2000= $ 9. 07 Total cost for Vanilla = $164486. 44 + $ 300000 = $ 464486. 4 And, per unit cost for Vanilla = $ 464486. 44/ 100000 = $ 4. 64 Question 2: What are the effects, if any, of changing the company’s costing method? Specifically, are the differences between the two costing methods material in terms of: a) Their effect on individual product costs? b) Their effect on total company’s profits? (assume no changes in any operating decisions, such as prices and production volumes) Ans 2 a & b: The change in ‘Costing Method of the products’ has significant impact on Costs of the products under observation (Polynesian Fantasy & Vanilla). How firm allocate Overhead costs across its product portfolio, can affect Firm`s Product Mix, and pricing Strategy.

In current method Overhead cost is allocated based on Direct Labour hours consumed for a product; but it reality Overhead cost is made of several individual activities which may or may not be directly proportionate to Direct Labour costs. Hence current Costing Method though simple, is less accurate and may narrate wrong picture of profitability of a product. In new method Overhead cost is divided into various activities and apportion based on consumption of the activity in producing the product. e. g. Quality Overhead costs are allocated based on ‘Number of batches’ of the product based rather than Direct Labour costs. Hence New method gives more accurate picture of the costs and hence profitability associated with the product.

The comparison of overhead costs allocation for both the products by the two costing methods is as under: | |Polynesian Fantasy |Vanilla | |Old Costing method |4800 |240000 | |New Costing method |11738. 70 |164486. 44 | |% change |144. 56 % |-31. 46 % | As a result, per unit total cost of both the products has also changed. The new costing method is more accurate as it allocates overhead cost appropriately and more accurately than the earlier costing method. Using the new costing method (Activity Based Costing), it is observed that Polynesian Fantasy is heavily under priced whereas Vanilla is overpriced. Results |Polynesian Fantasy |Vanilla | |Activity Based Costing |9. 07 |4. 64 | |Existing Costing Method |5. 6 |5. 4 | |Underpriced/ (overpriced) |- 61. 95% |13. 98% | Effect of Company’s Profit: Costing is an Internal process of the organization, and hence only by changing Costing Method there won’t be any change in profit made by company as a whole. However profitability of the individual product will have impact on it.

In this case, few products might show improved profitability, which will be compensated by decrease in profitability of few other products. Resultant Profits of the Organization will remain same. Question 3: What should Will do now? Explain. Ans: Proper allocation of overhead is possible through Activity Based Costing. Hence, in order to get more accurate cost of his products, Will should adopt Activity Based Costing. This will though not increase the overall profit of his company but will help him in closely analyzing various costs associated with individual products and can improve the manufacturing process and efficiency which in turn can increase the profitability of the company.

When a firm have multiple products which are consumes same overheads, products are produced in batches, and details of overheads along with the Cost Driver is identifiable, it is always advisable to used activity based costing. In current case Will have the information about details of the overhead cost and he should use Activity Based Costing Method. It will give exact cost of the products based on which Will can make future strategy for Ideal Product Mix, Marketing efforts, and firm’s profitability. After having new Costing method implemented Will should examine profitability of all products and redraw the strategic decisions in the light of more accurate cost information

California Creamery. (2019, Dec 06). Retrieved from https://paperap.com/paper-on-essay-california-creamery/